Our Newsletters

If you want to be added to our Newsletter Email list,

If you want to be added to our Newsletter Email list,

Contact Us and ask us to add you to our list.

All Systems are Go ... for Year 2026 (01-16-2026)

Chances are, at least half of the people reading this newsletter remember a familiar phrase NASA used when America was putting a man on the moon in the .....CONTINUE READING

Avoid the Next Stock Market Whiplash (05-21-2025)

During the market turmoil in April, we experienced a significant downturn in just a few days, followed by the fastest stock market rebound in 40 years. During this time, I received ......CONTINUE READING .

2024 Market Outlook Spring (03-28-2024)

Take the Win and Be Happy. Let's go out and enjoy the outdoors before the heat comes roaring in. We probably have about six to seven weeks. You know I look back on January 12th when I came out with my stock market prediction, which I do every year, which is a real ...CONTINUE READING

2024 Stock Market Predictions (01-12-2024)

In 1968, Yale Harsch introduced the concept, or the phenomenon, of the Santa Claus Rally. It was a rally held in the last couple of weeks of December. While it does....CONTINUE READING

Bank Bear Trap (03-16-2023)

We watched the regional bank industry experience a "Back to the Future" event. You remember the financial crisis when banks failed in 2008. Fortunately, it is not as bad as 2008, but perhaps it could have been avoided .....CONTINUE READING

January 2023 Barometer- Myth or Reality? (02-01-2023)

Drip, drip, drip. Before I get to the January 2023 Effect, let's just recap last year. As you probably know, nothing good happened in the markets. Jerome Powell (the Fed chairman) was renamed as a serial ...CONTINUE READING

Bear Market - How long will it last ? (08-09-2022)

Drip, drip, drip. I had a client last week tell me that this bear market just seems to drag on and on and on. She asked, “how much longer with this ....CONTINUE READING

Bear Market - How long does it take to Recover ? (6-24-2022)

"It was announced on JUne 14th, 2022, that we are officially in a Bear Market for the S&P500. The NASDAQ index was declared to be in a Bear Market almost ...CONTINUE READING

"Put the Lime in the Coconut and Drink it All Up." (4-29-2022)

"Inflation is funning Hot, here comes the Fed." ..."Is the Stock Market a Leading Indicator?"...Short Recession ?" What about Bonds ?" ..CONTINUE READING

Whoopty Doo. But what does it all mean..." (2-17-2022)

"I will get to this famous Austin Powers quote later in the newsletter. But if you remember my January newsletter, I emphasized how I expected a rockier market in 2022. Well, guess what ? That's what we have gotten so far. The market is currently in ...CONTINUE READING

Goodbye Year 2020 ! (1-6-21)

"Hit the road, Jack ! And don't you come back. No more, no more, no more, no more ! Hit the road Jack. And don't you come back no more..! " Ray Charles recorded this song in 1961 and I believe this song reflects how most ...CONTINUE READING

Economy - Recovering - Accelerating (8-20-20)

Certainly, the most frequently asked question I get is, how can the stock market be doing so well when things appear to be so bad ? ...Let us just focus on the stock market and this ....CONTINUE READING

April 2020 - Tough Month (4-3-20)

This may be the understatement of the year. Supposedly as we head into the peak or the peak of this coronavirus, I hope you are doing well.. this beark market is different because not only are people worried about their ...CONTINUE READING

Bear Market - Straight Talk (3-17-20)

During this recent market meltdown, I happen to look back and noticed that this was the sixth bear market that I've experienced...During this economic downturn, certain businesses are grinding to a ...CONTINUE READING

Stock Market Meltup OR Down? (5-10-19)(# 2535097.1)

What a difference a few months make. Perhaps I don't have to remind you of the market correction/bear market in the last quarter of 2018. It cumulated into what they call "The Christmas Eve Massacre." Traditionally, the market doesn't go dow a few days ...CONTINUE READING

Tax Man or Stretch IRA ? - Leaving a Legacy (3-28-19)

The stretch IRA concept, which I have implemented for almost 20 years, is truly one of the most powerful money/investment techniques that I know, that doesn't cost ..CONTINUE READING

Fiduciary Duty - Does your Planner owe it to you ? (2-28-19)

In 1968, Archie Bell and the Drells unleashed a hit song called “Tighten Up.” More about the song later. With market volatility hitting extreme levels in October and continuing into November, I'm fielding more calls, emails, and questions, not only from ......CONTINUE READING

Tighten Up Investor - Market Volatility (12-7-18)

In 1968, Archie Bell and the Drells unleashed a hit song called “Tighten Up.” More about the song later. With market volatility hitting extreme levels in October and continuing into November, I'm fielding more calls, emails, and questions, not only from ......CONTINUE READING

My 86-year old mother - weed stocks (07-19-18)

I bet you that title got your attention! A month ago I received a phone call from my mother and she asked me a question that I've heard multiple times from retirees over the last four or five years. How do I exactly buy some of these companies that are selling this marijuana? My mother said ....CONTINUE READING

Fed Raises Rates for the 7th Time (07-05-18)

I listened to our new Fed chairman, Jerome Powell, on June 13th, 2018. It was refreshing to hear the new Fed chariman speak in actual plain English. His predessors, both feds and economists, were so .......CONTINUE READING

I have met the World's Worst Investor (5-22-18)

Over the years, I have had many clients comment to me during our initial meeting claiming to be the worst investor. I have finally met the world's worst investor last week ! He was an aeronautical engineer and he creates and runs .......CONTINUE READING

My Favorite Chart (4-23-18)

I have used an updated version of this chart for 20+ years. It represents what a long-term structural markt looks like (sometimes called a secular market). I ahve received many questions about how long this bull market ....CONTINUE READING

Who Dunnit? February stock market (02-16-18)

You as an investor have witnessed stock market declines of 1,000-points in just the first week or so of February. It's been quite a while since we have seen this kind of ....CONTINUE READING

Can the 2018 Stock Market outperform 2017 returns? (01-15-18)

I don't think anyone can argue that the last year in the stock market was about as good as you could've hoped for. However, going into 2018,a week goes by when I do not field questions about what direction the market is heading....CONTINUE READING

What Kills a Bull Market? (09-29-17)

Not a week goes by when I do not field questions about what direction the market is heading. "The media pronounces that tomorrow at 9:30 sharp the market is going to crash." " The market is going down because of the presidential job approval." "The market is toast because of BREXIT." "The market is going to bust because of the .....CONTINUE READING

What is the Market cooking ?(08-24-17)

I A former professional wrestler called "The Rock" is on TV, movies, and Netflix. You pretty much can't go anywhere without seeing the personality of "The Rock." As a former wrestler, he had build his entire career on jumping up on the rope and getting the crowd psyched up by saying, "Can you smell what The Rock is cooking?" And now The Rock is thinking about running for president ! I will get back to The Rock in a little bits, but let's talk about ....CONTINUE READING

My Favorite Chart (05-19-17)

I have used an updated version of this chart for 20+ years. It represents what a long-term structural market look like (sometimes called a secular market). I have received many questions about how long this bull market can last, and I always reference this chart to show that structural markets last for a very long time. Let me elaborate a little more on that. When we look at the chart it says .....CONTINUE READING

“Houston, all systems go!” (03-22-17)

Do you remember when America was on the way to the moon? Or perhaps you were too young to have seen some of the Apollo missions/rockets (years 1961 - 1975). Back then, we only had three channels on the television and the whole nation watched the countdown to the major rocket launches (i.e. Apollo Missions). Luckily for me ......CONTINUE READING

One Chart that Explains it All (02-06-17)

It's all about growth in the economy, or lack of. Take a look below at the wonderful chart done by Oppenheimer that shows GDP (gross domestic product) since 1966 [1]. It presents an average of about 3% GDP growth. Well, in the last eight or nine years it has been subpar. Many of .....CONTINUE READING

Is It Morning in America ? (11-16-16)

My son Nick is in a one-year countdown to exiting college and going into the job market fulltime. He recently asked me if the election results could affect future employment opportunities. I said, "Nick, don't focus on politics. Instead focus on the ............CONTINUE READING

Bull Markets Don't Die of Old Age.... Recession (8-31-16)

I have been asked numerous times how long do bull markets last? Perhaps a pundit has been on television describing the reason why the market cannot go up, because the market has aged past the normal .......CONTINUE READING

----------------------------------------------------------------------------------------------

Chances are, at least half of the people reading this newsletter remember a familiar phrase NASA used when America was putting a man on the moon in the 1970s. As the Apollo rockets prepared for launch, television viewers would watch mission control go around the room, one system at a time, saying, “Fuel system status?” One by one, each team confirmed readiness by saying, “We are go.” It was methodical—and oddly exciting.

And then finally, the launch coordinator would declare, “All systems are go.”

Before we talk about the investment systems we have in place for 2026, let me get my annual market prediction out of the way. Each year, I revisit my prior forecasts to see how they held up. Last year, I projected a market return of roughly 12% to 13%. The year before that, I said we were still in a bull market and should expect bull-market-type returns. The good news is, we are still in a bull market. In fact, as I’ve been saying for the past couple of years, this may ultimately prove to be one of the greatest bull markets of the last 50 years.

SYSTEMS CHECK

Let's go around the room and see how the systems/business environment looks as of now.

Tax cuts are going to go into effect for literally millions of Americans spanning a broad cross-section of the population. Most importantly, at least from an economic standpoint, what's happening on the business side?

- Businesses can now deduct 100 percent of capital expenditure in year one. This has never happened before. It creates a powerful incentive for companies to immediately invest in factories, buildings, machinery, and other capital goods.

- Regulations that have historically slowed or paralyzed business activities are being rolled off the books very aggressively, which allows companies to move faster and operate more efficiently.

- Companies are onshoring production. COVID taught corporate America a hard lesson. Global supply chains spanning the world are neither reliable nor resilient. So, companies are onshoring back their production.

- Investing in America is accelerating. An example is Taiwan Semiconductor, the world's largest chip manufacturer, which is now committed to building a semiconductor foundry in Arizona and estimates it will invest as much as $300 billion(1). And folks, this is just one company of many coming here.

- The U.S. is leaps and bounds ahead of every country in artificial intelligence, including China. We are at least two to three generations ahead in advanced semiconductor chips.

- The race to build AI and data centers is creating massive job demand. Beyond direct employment in the data centers, the country is racing to upgrade the electric power grid, which many people say is going to create jobs for half a million electrical workers, linemen, electricians, and engineers, as well as hundreds of thousands of jobs in HVAC construction, mining, and energy jobs.

- When you look at data centers, they're kind of like the factory of the 21st century. What they do is convert energy into processing capacity.

- America is the largest energy producer in the world. I recently purchased gasoline for $2.49 a gallon, something I haven't seen in many years.

- The defense industry is ramping up both to rearm and to maintain America's military superiority.

- Interest rates are trending downward, unlike the increases that we saw from 2020 to 2023. This really matters. Home building is a crucial driver of the U.S. economy. Most homeowners who had 3% mortgages were never going to move just to assume a 7% or 8% mortgage. Lower rates should help unlock housing deand.

PRODUCTIVITY SURGE

The U.S. economy has been stuck in a 1% to 2% range of GDP growth for the past 10 to 15 years. History shows that when productivity rises, GDP rises, and company stock prices also rise. Let me repeat that.

Normally, when GDP rises, company stock prices also rise. The last major productive surge we had was in the 80s and 90s, driven by the internet.

Today, artificial intelligence has the potential to drive productivity gains on a scale we haven’t seen in decades. Yes, AI will disrupt certain jobs and industries—but change always does. Fax machines disrupted mail. Email disrupted fax machines. Kodak once controlled nearly 90% of the photo and film market—until cameras were built into phones. Innovation always creates winners and losers, but the net effect is higher productivity and stronger economic growth. I believe AI will have a meaningful impact on GDP. If you want to track it, watch GDP growth in the first and second quarters. I expect growth in the 3% to 5% range.

WRAPPING UP

I've been an investment advisor for decades, and I can honestly say that I'm having the time of my life. I bought my first investment when I was 15 years old. Investing was an interest of mine even as a teenager. Over the years, I've lived through multiple bull markets and bear markets, and each one has reinforced the same lesson. Know what market you're in and invest accordingly. As many of you know, I have no intention of retiring. My health is perfect, and I enjoy this business immensely. The truth of the matter is that this business, helping people create reliable income streams for retirement, is incredibly gratifying. And rest assured that I use the same strategies in my own personal accounts.

THANK YOU

I also want to sincerely thank you for being a client. I can't tell you how much pleasure I get from helping retirees achieve their goals. There isn't a week that goes by that I, or my staff, don't hear from a client or sometimes even their children, and you know what, we hear from their grandchildren expressing genuine appreciation for the help we've provided as well.

HEY, I COULD USE YOUR HELP

As many of you know, I don’t do traditional marketing—no seminars, mailers, or advertising. That allows me to focus on what matters most: investment research and working directly with clients. My team handles the day-to-day details, and I’m grateful for their support. Each year, I try to bring in about 6 to 10 new clients through referrals from people I already work with and trust. If someone comes to mind who might benefit from a conversation, I’d appreciate your help. This could be:

- An adult child whose net worth is largely in a 401(k) and receiving little guidance

- Someone nearing retirement and wondering how to create a reliable income

- A friend who recently lost a spouse who managed the finances

- simply someone dissatisfied with their current advisor.

We may or may not end up working together, but I can promise they’ll be treated with the same care, respect, and the professionalism you receive. Thank you for your continued trust and confidence. It truly means more to me than you know.

Sincerely,

John Romano, CFP®

Office Phone: 352-753-8590

Email: john@romanojohn.com

Address:

3261 US Hwy 441

Building D2

Fruitland Park, FL, 34731

Data contained in this newsletter is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed.

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Osaic Wealth, Inc. (a member of the FINRA and SIPC) and an Investment Advisor Representative with Osaic Wealth, Inc. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Osaic Wealth, Inc., a Member of FINRA/SIPC, John Romano, CFP® Registered Representative. Advisory Services are offered through Osaic Wealth, Inc., John Romano, Investment Advisor Representative. Romano Income Strategies and Osaic Wealth, Inc. are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by anyone who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

Avoid the Next Stock Market Whiplash

During the market turmoil in April, we experienced a significant downturn in just a few days, followed by the fastest stock market rebound in 40 years. During this time, I received several phone calls, including one from a client who asked, “John, why don’t you seem that concerned? I explained that my calmness stems from a few main reasons, which I will elaborate on throughout this newsletter.

First, it’s normal for markets to undergo one or two corrections each year and to enter a bear market every three to four years. This behavior is simply part of the cyclical nature of the market. Having worked in this business for decades, I’ve seen it often, much like observing a washing machine as it goes through its cycles: wash, rinse, spin, dry. During the spin cycle, it may seem like the machine shakes, but that’s just part of its normal functioning. Similarly, market downturns are expected; however, it’s crucial to determine if any underlying structural issues are causing these fluctuations.

Is There Something Structurally Wrong with the Economy?

During a market correction or bear market, the first question I always ask myself is whether anything is structurally wrong with the American economy. Many people have a vivid memory of the bear market of 2007-2008, when the real estate market essentially collapsed. At that time, millions of homes were purchased at exorbitant prices, and many homeowners could not pay their mortgages. Major banks, brokerage firms, and insurance companies were all interconnected, and as a result, they began to fail at an alarming rate. The whole system was in serious trouble due to these institutions being tied to assets that had lost their value. This caused a severe bear market, with unemployment soaring and millions of homes going into foreclosure. The Federal Reserve had to step in to support these institutions; without this intervention, the collapse would not only have continued but would have accelerated.

April Tariff Talks Stock Market Massacre

I cannot think of a better description of the downturn in April. It was all about tariff discussions—just back-and-forth, talk, talk, talk. People debated whether tariffs would have an effect or not. However, the key takeaway is that, beneath the surface of the American economy, there was nothing structurally wrong. Unemployment stayed at around 4 to 4.5%. Inflation has decreased. It seemed like the American consumer wasn’t too worried, as spending continued. Yet, the market experienced a significant downturn due to all this chatter.

This situation was similar to what we saw during COVID in 2020, when the stock market faced a bear market that lasted only two or three months. There was nothing fundamentally wrong with the economy then; the government had simply shut it down for a couple of months. Once everything reopened, the economy bounced back rapidly. So, let me reiterate that not only did we recover from the market downturn in April, but we also recovered from the prior challenging months earlier this year when the market was declining. Again, there was nothing structurally wrong.

Another main reason I remain untroubled is that, alongside the macro environment we’ve just discussed, I have been using a technical analysis methodology for investing for the past 27 years. Many of you have seen how our system works over time. You typically receive a call from me every three or six months, or you may visit my office, where I advise making adjustments to focus on the stronger sectors of the market. Our goal is to remain invested in the top-performing sectors. Yes, when the tide goes out, it affects everyone, but we can still ensure we are invested in the best sectors at any given time.

My analysis of the most effective sectors is based solely on performance and pricing metrics. I do not speculate regarding future trends or the potential impact of tariffs on any specific sector. My primary focus is on identifying what is currently prospering - namely, what has demonstrated effectiveness over the last week, month, three months, and six months.

It’s important to note that while one cannot accurately time the market, it is possible to reposition investments toward the strongest sectors at any given time to optimize the likelihood of success in both favorable and adverse market conditions.

401(k) – Need Help?

With respect to 401(k) plans, I frequently encounter younger clients who express the following sentiment: “John, I have invested with you, but a significant portion of my funds remains in my 401(k).” I strongly advocate for 401(k) plans, particularly when accompanied by a company matching contribution. However, a notable concern arises when individuals possess one of their most substantial assets, if not their largest investment asset, without appropriate management. Employers typically provide a limited array of investment options but offer minimal guidance. Consequently, many individuals, especially those actively employed, tend to lack the time to monitor their investments closely, as their primary income is derived from their jobs. Ultimately, they often select a few subaccounts and neglect them for years or even decades.

I encourage individuals to contact me regarding their assets that my firm does not currently manage. Despite the limited investment choices, commonly ranging from 10 to 30 subaccounts, I would be pleased to review these options and recommend which sectors may be worth considering for reallocation. This review process requires minimal time on my part.

Prepare for Upcoming Hurricane Season

On a related note, as we approach June, I would like to remind everyone that hurricane season is imminent. I sincerely hope the West Coast of Florida will not experience further devastation. Areas such as Crystal River, Sarasota, Fort Myers, and Englewood have been significantly impacted over the past three years. It has been observed that hurricanes tend to follow cycles lasting approximately 5 to 10 years. I recall instances in the past when storms that threatened Florida would divert and strike New Jersey. At the same time, for a period of 10 to 15 years, they would instead travel south of Cuba and impact Louisiana or Mississippi. While I do not wish to displace the impacts of hurricanes onto other regions, I do hope that the residents in those areas receive respite for at least the next few years. In light of the rising property insurance costs, it seems likely that individuals may be compelled to relocate.

Thank you, as always, for listening to my thoughts, and I hope you enjoyed this newsletter.

Sincerely,

John Romano, CFP®

Office Phone: 352-753-8590

Email: john@romanojohn.com

Address:

3261 US Hwy 441

Building D2

Fruitland Park, FL, 34731

Data contained in this newsletter is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed.

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Osaic Wealth, Inc. (a member of the FINRA and SIPC) and an Investment Advisor Representative with Osaic Wealth, Inc. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Osaic Wealth, Inc., a Member of FINRA/SIPC, John Romano, CFP® Registered Representative. Advisory Services are offered through Osaic Wealth, Inc., John Romano, Investment Advisor Representative. Romano Income Strategies and Osaic Wealth, Inc. are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by anyone who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

Take the Win and Be Happy

Let's go out and enjoy the outdoors before the heat comes roaring in. We probably have about six to seven weeks. You know I look back on January 12th when I came out with my stock market prediction, which I do every year, which is a real gamble, but I went ahead and committed it to paper. I said I thought we would end up with an 8% to 12% return for 2024. So far, right on target. I want to go back and rehash some of the indicators that I mentioned back in January https://www.romanojohn.com/Our--Newsletters.11.htm for reasons to be happy about the market. And then I'm going to talk about some new ones.

• Federal Reserve Policy: The Fed is expected to continue lowering interest rates, which is seen as positive for the stock market.

• Impact on Industries: Lower interest rates are expected to stimulate demand in various industries related to housing, such as construction, manufacturing, and home appliances.

• Impact on Investments: With the Federal Reserve easing, yields on money market accounts, CDs, and savings accounts are likely to drop, potentially leading some investors to allocate more funds into the stock market.

• Stock Buybacks: a move that could reduce the supply of available stocks and potentially drive-up prices, making it an opportune time for investors. Expected buybacks are up to 1 trillion this year. (1)

• Wealth Effect: Positive stock market performance and increase of housing values tends to stimulate consumer spending, further boosting the economy.

I’ve Saved the Best for Last

Thanks to advancements in artificial intelligence, I'm witnessing anticipated boosts in productivity that border on the incredible. We're talking about achieving productivity gains in the double digit. Ordinarily, the U.S. economy sees growth rates of 2% to 3% annually, but projections indicate a significant surge beyond that range. While the exact extent of this growth remains uncertain, it's expected to mark the most substantial productivity leap for American workers since the internet. I do know that when companies enhance productivity, profits follow suit, ultimately propelling market dynamics.

Reflecting on my own journey, I recall being advised early in my career that I wouldn't reach my full productivity potential until I enlisted assistance to handle administrative tasks. Taking heed, I promptly acquired such support. Consider, if you will, whether you're now retired or if you have conversations with younger generations, the pervasive challenge of administrative burdens faced by many Americans. They often find themselves mired in paperwork and tasks they'd rather not undertake. Imagine the potential productivity gains if everyone had access to one or two assistants.

While such resources might not have been feasible in the past due to various constraints, the advent of artificial intelligence raises intriguing possibilities. Could AI provide virtual assistants to alleviate mundane tasks for everyone? I know I couldn't do what I do without my administrative help. And this is where the productivity is going to come in. It will be great to see.

Many Thanks

I wanted to thank you all for the great referrals. Back in January, I mentioned that we wanted to bring in some new clients, and I think we had a target of 24. And we have done about 40% of that. And that's all thanks to you! You referred us to some of your kids, and your friends, and we really appreciate that. Let's take the stock market wins in 2023 and 2024 and be happy. Have a great spring!

Best Regards,

John Romano, CFP®

Office Phone #: 352-753-8590

Email: john@romanojohn.com

References:

1. https://www.vox.com/future-perfect/24108787/ai-economic-growth-explosive-automation

Data contained in this newsletter is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed.

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC) and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored.

Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential, and use by anyone who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

Santa Claus Delivers/John's Predictions for 2024/Hey, I Need Your Help...

In 1968, Yale Harsch introduced the concept, or the phenomenon, of the Santa Claus Rally. It was a rally held in the last couple of weeks of December. While it does not work every year (nothing does), it sure worked this year. The long-term investor in 2023 who did not get head faked out of the market was rewarded as they should be.

John's 2024 Prediction

Well, it's about that time when everybody starts making their stock market predictions for 2024. Well, here's my two cents. The market's going to go up, and it's going to go down. Hey, I can't go wrong with that one, right? Keep reading on to get the real prediction.

Data points

Based on data points, not your Aunt Nervous Nelly, who tells you over the holidays every year that the stock market is going to crash and it's going to be like the Great Depression. Instead, let's look at some recent data points:

• Interest rates are not only not going to be rising, but they will be actually going down. I believe this will stimulate the housing market because there is so much pent-up demand. People weren't moving and weren't buying because of the close to 8% mortgage rate, but I believe as rates get closer to 5 or 6%, they will.

• Also, the ancillary industries that are directly related to the housing market, whether it's construction, manufacturing, furniture, concrete, timber, copper, refrigerators... these industries will pick up, and unemployment will go even lower.

• Speaking of unemployment, it's already historically low, and you know what they found about the consumer? As long as they have no fear of losing their jobs, they will keep spending.

• This is the real biggie. The Fed is seemingly not going to be raising rates, but indeed, the prediction is to lower rates two to four times this year.

• The onshoring boom of bringing back factories to the U.S. is up, and last year, it's up a staggering 71% year over year, and over a two-year period, 131%. COVID taught us that we not only need to shorten the supply chain but also to move more of these important factories back to this country.

• Small and mid-cap stocks have joined the bull market party, which leads to a much broader market.

More importantly, I believe the fear of COVID has faded. Now, I'm not downplaying the severity of the virus. But after having it and watching everybody I know have it at least one time in 2023, we have just learned to live with it. The morbidity of sheltering in place, hiding in your house, being scared to even talk to people, much less going outside, had a tremendous effect on the psyche.

Just the optimism of going out and living life, enjoying the activities, can’t help but improve your optimism. If you're going to be an investor, you're normally an optimist, thinking that you're going to be around sometime in the future to enjoy these funds. But if you are at home, sheltered in place, scared to move, it leads to some real pessimism, which I think is bad for investing. Now, I could be off base on this, but I don't think so.

Age of Aquarius

I heard this song called Let the Sunshine In over the holidays by a band called the 5th Dimension. They were talking about the stars and moon being aligned. [1]

VERSE: When the moon is in the Seventh House, And Jupiter aligns with Mars, Then peace will guide the planets, And love will steer the stars

CHORUS: This is the dawning of the age of Aquarius, Age of Aquarius, Aquarius, Aquarius

My Final Prediction

I’m not sure if the stars and moon are aligned, but I think the data points for a good stock market in 2024, so here you go, drum roll, please... My prediction of the market return is 8 to 12%.

Thankful

You know, it seems like over the holidays, I always run into an investment advisor whom I've known my whole career. He's about ten years older than me, and our conversation always centers on how lucky we both are to be in this investment advisory business. There's no thought of retiring for him or for me. It's a great business, not only monetarily but also because it allows me to do the things I want.

Over the decades, I've had the chance to help hundreds if not thousands of retirees to live not a worry-free retirement (because there's no such thing) but worry less about their biggest fear, which is running out of money. And I know this because my clients tell me this on a weekly basis. Indeed, I get calls and letters from their loved ones saying things like thanks for taking care of my mom or dad. Furthermore, some of my clients are in their seventies and eighties, and I normally do three-way calls with not only them but also their children. Their children want to be involved, but they're probably at the peak of their careers right now, and they're probably still raising their own families. It's just comforting to them to know that somebody is down here looking out for Mom or Dad. So, thank you greatly for letting me serve you.

I need your help.

Hey, I need your help. As many of you know, I get all my business from referrals. I've told the team in 2024, I think I'd like to bring in about 20 or 24 new clients. So, if you know:

- One or more of your children who have the bulk of their net worth in a 401k and are getting no help.

- Somebody you know is getting ready to retire, and they are wondering how to create income streams.

- A friend who just lost a spouse who took care of all the financials.

- Any person that you know who is not happy with their current advisor.

- If you have a good candidate call Margaret at our office, or email us.

Please send us the contact information so my office team can reach out to them. We may not do business with them, but we will treat them like we treat you.

It may not be the age of the Aquarius, but let’s have a great year!

Sincerely,

John Romano, CFP®

Office Phone #: 352-753-8590

Email: John@RomanoJohn.com

Data contained in this newsletter is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed.

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC) and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential, and use by anyone who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

References:

[1] https://genius.com/The-5th-dimension-aquarius-let-the-sunshine-in-lyrics

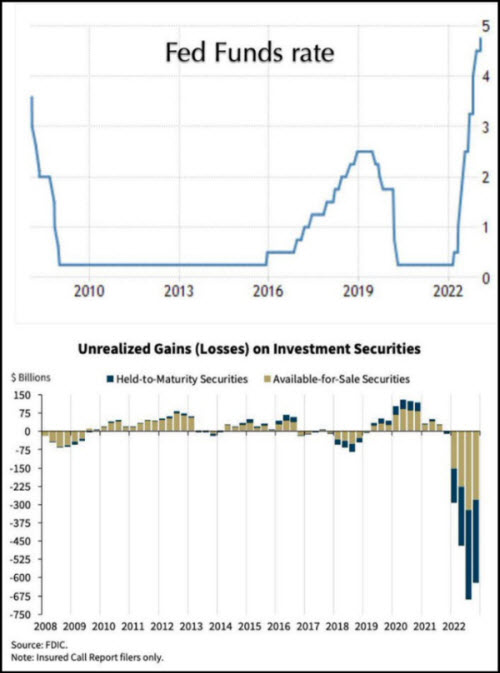

We watched the regional bank industry experience a "Back to the Future" event. You remember the financial crisis when banks failed in 2008. Fortunately, it is not as bad as 2008, but perhaps it could have been avoided. Make sure you read the last section of this newsletter because there is some good news.

Janet Yellen, the treasury secretary, whose job is to monitor the bank industry, just a few days before the crisis unfolded on March 10th, spoke at a climate conference. Her presentation said that climate change would likely become a source of shocks to the financial system in the coming years(1). While she's up there talking about the weather, the banking industry actually had a financial shock. In essence, there was an old-fashioned run on the banks because of facts, not rumors, getting out that some regional banks had more liabilities than assets.

In the SVB case, they were the first bank that experienced a known problem and had received so much money and deposits in 2020, 2021, and 2022 that they were out buying 10-year treasuries. Unfortunately, these 10-year treasuries, the yield was 1.5%(2). So, the Fed starts raising rates like they had talked about for a couple of years, really in 2022, and as most people know, when interest rates rise, the principal value of bonds drop. You may wonder why the banking industry was covering, in essence, one-day deposits with 10-year bonds. In other words, if your depositors wanted their money, you had to sell those bonds at a loss.

Please see the chart below from an article by David Sacks(3). His illustration better explains what's going on with the banks than anything I've seen. This illustration shows the banking industry's bond portfolio on the bottom and how much value it lost as the Fed raised rates(top of the chart). Losses are in hundreds of billions of dollars.

The Four Steps to the Banking crisis:

Step #1: The government prints and passes out free money to anybody who can fog a mirror, plus passes multi-trillion-dollar spending bills, which causes the worst inflation we've seen in 40 years.

Step #2: To combat inflation, the Fed raised rates very aggressively, driving down the principal value of the bonds banks had purchased.

Step #3: This made a few of the banks technically insolvent. If there was a run on the banks - oops.

Step #4: Yes, Mildred, there was a run on the banks.

No Soft Landing Here

Chairman Powell has been saying for months that they are hoping to have a soft landing, which equates to raising rates enough to lower and calm inflation without triggering a monetary crisis. Well, you can't really say mission accomplished with this one!

Fortunately, the government will step in and ensure no depositors are hurt, regardless of the amount they hold at a bank. Banks will be forced to tighten up, and their costs will increase due to having bailed out the few affected banks. Banks will have less money or will be more reluctant to loan money. Currently, 30% of the loans in the country are done by regional banks(4). Do you expect more loans or fewer loans? I expect fewer loans, so we'll have less economic activity. But hold on; there might be some good news for you.

Hidden Gem

It’s time to go long. Believe it or not, there's a gem in the coal mine caused by the fed raising rates. It may be time for you to go long with certain investments. Specifically, I'm talking about fixed income, whether a bond for three to five years, a CD for one to four years, or even a multi-year guaranteed fixed annuity for two to seven years. It's been many years since I've discussed this concept of going long. The last time was back in 2007 - 2009, and interest rates peaked in that business cycle. At that time, you could get 5- 7% on the above-mentioned investments and lock in a maturity date of 2 -5 years. Then we saw rates decrease for years.

Why do you need to go long? It’s not just football terminology. Going long refers to a maturity that exceeds one year. You go long if you think interest rates will decline or the economy is entering a period of uncertainty. Consider going long to lock in a decent return. I believe we'll see rates start going back down in about a year and a half.

Right now, the sweet spot on these kinds of investments looks anywhere from one to four years. Of course, every investor's situation is different. You can't just willy-nilly and go out and take advice from a newsletter without consulting with a qualified investment advisor. As always, please feel free to call me with any questions.

Sincerely,

John Romano, CFP®

Office Phone #: 352-753-8590

Email: john@romanojohn.com

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

References:

(1) https://home.treasury.gov/news/press-releases/jy1325

(2) https://gulfnews.com/special-reports/biggest-bank-collapse-after-2008-global-recession-how-svb-spectacularly-failed-after-rate-heresy-becomes-reality-1.1678543355308

January 2023 Barometer Effect - Myth or Reality?

Before I get to the January Effect, let's just recap last year. As you probably know, nothing good happened in the markets. Jerome Powell (the Fed chairman) was renamed as a serial inflation killer. His mission impossible, which he decided to accept, was to raise rates to kill inflation and hopefully have a soft landing.

It was tough on almost all areas of the markets with the Fed raising rates very aggressively, there was no place to hide if you owned almost any asset class. Equity markets took a beating, bond markets had a tough year, real estate properties declined, and even Bitcoin took a major beat down - the tide was definitely going out. So long 2022, it's good to see you go.

With the purge of last year's market, is there a light at the end of the tunnel? So far in the month of January with positive returns in the 4% to 5%, have we turned the corner? Let's talk about the January Barometer Effect. The January Barometer Effect was first discussed by Yale Hirsch in the seventies. His study, which was just updated in 2022, showed for the last 50 or so years, that if the market had a positive return in January, it predicted a positive return for the year.

Here is what I expected:

- In 2022, we had a bad market in a decent economy.

- In 2023, we expect a worsening economy in a decent market.

- New market leaders will not be the big tech companies (Google, Facebook, Amazon, Netflix) but more big industrials, Boeing, Caterpillar, and John Deere.

- China's economy will tank for the next three to four months as Covid takes a massive toll, but their economy should start expanding toward the end of summer.

- International markets have started out with the best year we've seen in the last 10 or 15 years.

- Bond yields are looking rather well.

- We will probably not have a soft landing.

- Home prices will, and have probably already dropped around 15% to 20%, but there will not be a 2008-2009 collapse because of lack of supply.

- Demand will continue to cool for all high-ticket items that require financings such as homes, boats, and RVs.

- Ukraine could be the wild card if there's not a negotiated settlement soon.

As always, my job is to rotate portfolios in the right sectors, but the tide is coming in this year, unlike last year when it was definitely going out. So far, so good.

Best Regards,

John Romano, CFP®

Office Phone #: 352-753-8590

Email: john@romanojohn.com

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend, and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future result.

Bear Market- How long will it last ?

Drip, drip, drip. I had a client last week tell me that this bear market just seems to drag on and on and on. She asked, “how much longer with this Chinese water torture?” My response was, “well, I’m not too sure about this Chinese water torture thing, but I and most investment advisors are watching the Fed's next two or three rate raises - as the next opportunity the Fed can raise rates would be in September, November, and possibly in December.” I believe that after these three rate raises, they will have sufficiently raised rates enough to slow the economy down, and with it, inflation.

The economy is already slowing down. Home sales are going down, car sales are going down. Even Walmart is complaining that they're not able to sell merchandise on their non-produce side of the store. As mortgage rates have hit a 15-year-high, home sales and new home starts have dropped very significantly. It's interesting to me, that if you look at some of the car lots 7 - 8 months ago there were no new cars on the lots, and now you noticed the lots are starting to fill back up.

When do bear markets end? Well, Mark Hulbert published an article, CLICK HERE ON THE LINK TO READ:

He studied multiple bear markets and their correlation to the Fed rate rise. He noticed in the last six bear markets, that the market bottomed out 2 months before the last Fed rate rise. He also studied the performance of the stock market after the bottom. Ultimately, the average 1-year return of the S&P500 after the market bottomed was 25%. I believe the last rate hike will be in December, so it is possible the market will find a bottom and course in October.

The biggest wild card out there today is Europe because to quote a phrase from the HBO series Game of Thrones, “Winter is coming.”(2)

Energy prices have quadrupled in Europe primarily for two reasons, Putin's control of the natural gas pipeline and our dependency on green energy. I believe energy costs will not only make it a challenge for the industry, but I think that this winter we will see wholesale rationing. Europe is looking at a much more intense recession than we face.

Riddle me this. Since California has announced the phase-out and the complete ban on gas combustion automobiles in 2035 – how is this going to work? California now has about half a million electric vehicles with about 22 million gas autos. Over Labor Day, because of the power outages, they asked people not to charge their electric vehicles. If the electric grid cannot handle half a million vehicles today, then how in a few years can it handle 25 million? The answer is it can’t!

Don’t fight the Fed. When it is all said and done, I believe that the Fed is on the right course of raising rates. It will in all (most likely) worsen the economy. However, I think most Americans would rather have a short-term worsening economy versus multiple years of high single-digit inflation.

Best regards,

John Romano, CFP®

Office Phone #: 352-753-8590 Email: john@romanojohn.com

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

References:

(1) The stock market typically bottoms before the end of a Fed rate-hike cycle. Here's how to make that bet pay off. - MarketWatch

(2) https://ew.com/tv/2019/03/27/game-of-thrones-best-quotes/

Bear Market- How long does it take to recover ?

It was announced on June 14th, 2022, that we are officially in a Bear market for the S&P 500. The NASDAQ index was declared to be in a bear market almost 3 months ago.

Personally, this is my fifth or sixth bear market as an investment advisor and I can't remember one of these bear markets as being fun for anybody.

There is hope, but first, let's talk about what got us here.

- The government passing out trillions of pre-monies over the last two or three years.

- The Fed cutting rates to zero and pumping trillions of dollars into the economy.

- Threatening oil companies make it harder to borrow money to bring on new production.

- The war in Ukraine.

These four factors, plus a few others have led us to the highest inflation rate we have seen since the 70s. One of the new pastimes in America is when you were on your way to work to check out the oil prices and on the way out you check to see if they had gone up very much. So, America is witnessing the highest inflation that we've had in this country since the late 70s.

Jerome Powell (inflation killer)

Well here comes the inflation killer Jerome Powell 'The Fed Chairman'. He is aggressively raising rates to shut off demand. This is the only tool that the Fed has left to fight inflation. You must shut off demand for high ticket items which people were borrowing money on at almost not zero rates, but close to that.

Home Prices for example. Just three or four months ago you were able to get a 30-year mortgage at a rate of 2.90%, now that same 30- year mortgage rate is close to 6%. So, raising rates will shut off demand for big-ticket items - whether it's a home, a boat, a second home, a car, or anything where people normally borrow money and pay for it over time.

Unfortunately, when you shut off demand for these kinds of items, unemployment goes up. And then what normally follows that rise is a recession. The signal of a Recession is having two-quarters of GDP being negative or zero, and we've already done that in the first quarter, who knows where we're at in the 2nd and 3rd quarters.

Good news

As soon as the Fed see these rates taking effect going forward and shutting off demand, they will not be as aggressive in raising rates or maybe even slow the whole process.

What to expect from the stock market?

The average bear market lasts anywhere from 7 - 9 months. The method to count the time in a bear market is once a bear market is declared(June 14th S&P500) you go back and start counting the months the market started going down. In this case, it was January of 2022, so we will already be at month 6 or 7 therefore we are much closer to the end than the beginning.

In 10 of the last 12 bear markets, if you would have bought the S&P500 the day that a bear market was declared, you would have averaged 22.7% in the next 12 months(1).

The stock market is always 6 - 9 months ahead of the economy. And this year when the market started to go down, in January, it was spot on. Again, this is a Fed-induced recession whereas demand and prices dropped, the chairman will slow the rate hike.

One last caveat.

In the Bank of America article published June 17, 2022, by Barbara Kollmeyer, she explained that in the next phase, once the bear market stops, then a bull market starts. The average bull market lasts about 64 months, and she is projecting “the S&P will be at 6,000 by Feb. 28th”(2), almost a double from here.

Remember what sectors lead the last bull market almost never lead the new one.

Best Regards,

John Romano, CFP®

Office Phone Number: 352-753-8590

Email: John@romanojohn.com

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

References:

- https://www.marketwatch.com/story/those-who-buy-stocks-the-day-after-the-s-p-500-enters-a-bear-market-have-made-an-average-of-22-7-in- 12-months-11655224023

- https://www.marketwatch.com/story/based-on-history-the-next-bull-market-is-just-months-away-and-could-take-the-s-p-500-to-6000-says-bofa- 11655475414?mod=search_headline

“Put the Lime in the Coconut and Drink it All Up." -Baha Men (1)

Do you remember the song Put the lime in the coconut? It was originally released in 1972 by Harry Nilsson and redone by the Baha Men. The narrative of the song presents a woman who had a stomachache late in the evening, and she called her doctor. He didn't want to see her, so he told her to put the lime in the coconut and drink it all up. You may be wondering what this has to do with the stock market.

Before I dive into more details about the lime in the coconut miracle fix. I wanted to mention something I saw a few weeks ago on CNBC. It stated that 81% of Americans believe the U.S. will experience a recession within this year. (2) I was shocked because normally they go out and poll 100 different economists and come back out with all these realms of data. Their findings would be very inclusive because they would straddle the fence. I believe this poll done by asking the average American is spot on because many of them are driving by the gas station wondering what gas is going to cost this afternoon. They're going to Publix or Walmart for their groceries, wondering if they're going to spend $200-300?

People have been priced out of home buying because the average house has gone up 20-25% in the last year. And if they can't afford to buy a home, their rent has gone up 20%.

Inflation is Running Hot, Here Comes the Fed

So, Fed Chairman Powell is now going to crush inflation without crashing the economy. In Fed lingo, this means engineering a soft landing. He's going to put the lime in the coconut by raising interest rates. His goal is to shut off demand, which should cool inflation very quickly. It will be very interesting to see if he's able to engineer a soft landing.

For example, if you bought a home a year or so ago, I believe the average house price was about $350-370,000. Your mortgage rate was 2.95%. Fast-forwarding to today, the average home price is $440,000 and your mortgage rate is now 5.4%. So now you're going to spend almost two percent more on an interest payment on a higher purchase, which equates to serious money.

Chairman Powell’s goal is to raise interest rates, which will shut off demand and maneuver to a perfect landing. To put this in a simple context, the American public will now say, I'm just not going to pay that, whether they're looking to buy a home, a car, or a new computer system.

Is the Stock Market a Leading Indicator?

Yes, it is my belief that the stock market as a whole is a leading indicator. Think back to our last recession, which was just two short years ago in year 2020, except the last two years have been anything but short. They seem more like two long years. If you can recall, the market had started going down in the first couple of months of 2020, and then finally, we had the pandemic and pandemic-induced recession. Now, that recession was very short-lived. Even though the market had dropped 25-30% in just a couple of months, by the end of the year, the stock market had not only recovered the losses, but the S&P had a pretty good return of 18%.(3)

Short Recession

I believe this will be a short recession because it's a Fed-induced recession. Once they see demand drop, inflation should move down rather quickly, and they can stop raising the rates. While they can't turn this big economy around overnight, they can certainly point it in the right direction. New home sales dropped in March by about 9% from the prior year. I was talking to a banker the other day, and he had said they had started laying off mortgage brokers. I was also talking to a boat salesman, and he said up to the last month or two, you couldn't get any inventory, and now there's nobody in the showroom.

So maybe the higher interest rates have already taken effect. Furthermore, I believe a huge factor is consumer sentiment, and it is way down. And that's understandable. By seeing all these costs go up, people just are making up their minds, and they're just not going to buy that item. Obviously, they must pay for certain things, but nobody's forcing them to spend money on discretionary/luxury items.

Negative GDP Numbers Just Came Out

For the first quarter of 2022 negative GDP numbers were reported for this period of time. This is the first negative GDP numbers we've had since the second quarter when the pandemic had shut the country down. Now, don't worry, the same people who said inflation was transitory say they are not concerned about a recession.

What About Bonds?

I've had a lot of questions about bonds lately. Unfortunately, you can't buy bonds at this time because as interest rates rise, bond values drop. Fact is, the S&P is down about 15-16% as of the end of April. And the average, high-quality bond is down about the same percentage. Bonds react very negatively to rising interest rates.

So, What Have I Been Doing?

I've spent the last 4-5 months repositioning portfolios away from large growth companies which do terrible during recessions. The stock market has been pricing that in by going down on these particular sectors. Growth has been the best sectors for many years. Well, it isn't anymore. The good news is there are other types of companies, which most people would characterize as consumer durable companies, such as utilities, energy companies, grocery stores, auto parts stores, railroads, and health care, which are doing just fine.

So, Dr. John says has put the lime in the coconut and maybe add some rum and drink it all up. And as always, I stand ready to make changes to your portfolio based on the current conditions.

Sincerely,

John Romano, CFP®

Office Phone Number: 352-753-8590

email: John@romanojohn.com

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years of experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities are offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services are offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

References:

1. https://genius.com/Baha-men-coconut-lyrics

“Whoopty Doo. But what does it all mean...”– Austin Powers (2)

I will get to this famous Austin Powers quote later in the newsletter. But if you remember my January newsletter, I emphasized how I expected a rockier market in 2022. Well, guess what? That’s what we have gotten so far. The market is currently in a correction, I believe it started about the second week of January.

Corrections are normal

In fact, there have been 26 market corrections since WWII but with an average decline of 13.7%. The average recovery time in a correction is about three months.

The market is resetting itself for the future, interest rate hikes are coming, and the Fed is going to be shrinking its balance sheet. In English, this means the Fed is no longer going to be pumping trillions of dollars into the system while the government is handing out trillions of dollars of free money.

In 2021, with all this money flowing through the system and people spending it, it provided a tailwind for the economy. Think back, a lot of the people have been locked down for a year or two, and they were itching to get out and spend their money. People were bidding up the prices of homes as well as the prices of cars.

Unfortunately, now the party's over with.

Inflation is running hot, and I mean it is sizzling.

As a sidebar, if you discuss inflation was somebody under the age of 45 or so you might receive a blank stare because we have not had high inflation since the late ’70s. Well, for Millennials and Generation Z, school is in session. What is inflation? In a nutshell, inflation is when you're driving to work in the morning and you have half a tank of gas, but you feel like you need to fill up now because gas prices will be up later in the day.

"If it looks like a duck, walks like a duck and quacks like a duck, it's probably a duck”. - Albert Einstein.

Yes, I know Albert Einstein did not say this, but I may be going out on a limb here but some of the indicators are flashing recession in 2023.

Indicators:

- Billionaire bond investor Jeffrey Gundlach said, “Consumer Sentiment plunged on Friday to a fresh decade low, and that’s been a reliable leading indicator as to where the economy is headed in the future.” (1)

Normally when people have a bad feeling about the economy, they tend to not spend as much money.

- James Ballard of the Federal Reserve said on Valentine's Day, “I do think we need to front-load more of our

planned removal of accommodation than we would have previously...”(3) He supports raising interest rates by a full percentage point by the start of July and it appears he also wants to have 3-5 others this year.

- Bullard’s plan involves spreading the increases over three meetings, shrinking the Fed’s balance sheet starting in the second quarter, and then deciding on the path of rates in the second half based on updated data. (3)

- No more free government money will be passed out this year.

- The 10-year Treasury yield from January went from 1.5 to over 2% in one month.

The reason I see a recession in 2023 is because the Fed is going to be raising rates very aggressively. It has been my experience over the years that it takes eight or nine rate rises to really shut off demand. For example, do you think many homeowners today that are sitting in a house paying a 3% mortgage would move across town if the new mortgage rate was 6%?

Whoopty Doo, what does it all mean…?

If you were an Austin Powers movies fan, whenever he got a lot of data points, he would blurt out of

frustration, “Whoopty Doo, what does it all mean...? (2) Well, basically it means we're in a rising interest rate environment, probably headed in a recession in around two years.

The bad news

- Interest rates are heading up.

- Some stock market sectors are going to underperform. And indeed, some companies with business models predicated on low-interest rates probably won't be around here in a couple of years.

The good news

- You will probably see a little better rates on your savings/checking accounts.

- Prices will come down and so will inflation. Some stock market sectors are going to not only do well but flourish in this environment.

- Companies that have reasonable business models with products that people will need will move to the forefront - think energy, transportation, consumer staples, banks, agriculture, commodities, and utilities.

The proper way to deal with not only this correction but more importantly, the economy, is to consistently rotate into the sectors that outperform in that kind of environment. My job is to find those sectors and rotate in. But this is exactly how I've been managing my clients' accounts for years.

Sincerely, John Romano, CFP®

Office Phone Number: 352-753-8590

Email: John@romanojohn.com

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years’ experience in the financial field. John is a Registered Representative with Securities America, Inc. (a member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated. Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated. Guarantees are based upon the claims-paying ability of the insurance company. Past performance does not guarantee future results.

References:

- https://markets.businessinsider.com/news/stocks/jeff-gundlach-economic-recession-possible-this-year-consumer-sentiment-weakens-2022-2

- https://viebly.com/austin-powers-quotes/

https://www.bloomberg.com/news/articles/2022-02-10/fed-s-bullard-backs-supersized-hike-seeks-full-point-by-july-1/ https://markets.businessinsider.com/news/stocks/fed-rate-hikes-front-load-james-bullard-inflation-credibility-cpi-2022-2/ https://www.livemint.com/economy/feds-james-bullard-supports-raising-interest-rates-by-a-full-point-by-july-11644549964159.html

https://www.bloomberg.com/news/articles/2022-02-10/fed-s-bullard-backs-supersized-hike-seeks-full-point-by-july-1/ https://markets.businessinsider.com/news/stocks/fed-rate-hikes-front-load-james-bullard-inflation-credibility-cpi-2022-2/ https://www.livemint.com/economy/feds-james-bullard-supports-raising-interest-rates-by-a-full-point-by-july-11644549964159.html

The year 2019 was an easy year to be an investor and It was an even easier year to be an investment advisor! The tide was coming in. The wind was at our back. The fish were really biting - It was hard not to have great investment returns.

And, well, 2020 was a whole lot of different. Not only were the fish not biting, but the tide was also going out and we had a category five hurricane that was blowing at us, that came out of nowhere! I find it hard to believe that many people did not have a few, if not many, sleepless nights in 2020 worrying about themselves, their family, and their loved ones.

From an investment advisor’s perspective, it once again proved to me that you better have and utilize a rules-based investing plan.

Last year's headlines between the pandemic, the election, and the economy, I had some perspective investors that told me they were sitting there in cash or running for cover. 2020 was not as quite as good as 2019, but still in my book gave a solid investment return. Anytime you can get close to a double-digit return it is a win. If you can get that kind of return while it seemed like your very way of life was going to be changed forever - Then it's a double win! If nothing else went right for you in 2002, at least the market performed.

RULES-BASED INVESTING